Markets dropped in March as rising concerns about the ongoing hostilities in the Middle East weighed on investors. Rising energy prices and interest rates during the month challenged bond returns, and both domestic and foreign stocks ended the quarter in the red.

Beyond the Headlines: Markets Fall to End Quarter

Markets fell in March, driven by rising geopolitical uncertainty due to the ongoing war in Iran. The S&P 500 fell 4.98 percent in March, which led to a 4.33 percent decline for the quarter. The story was similar for the Dow Jones Industrial Average, which dropped 5.20 percent in March and 3.19 percent for the quarter. Technology stocks were hit especially hard during the quarter, as rising concerns about the disruptive nature of AI weighed on technology companies to start the year. The Nasdaq Composite fell 4.68 percent in March and 6.96 percent for the quarter.

These disappointing returns came despite improving fundamentals. Fourth-quarter earnings season recently wrapped up, and the results were impressive. As of March 20, with 100 percent of companies having reported actual earnings, the average earnings growth rate for the S&P 500 was 13.2 percent. This is well above analyst estimates for an 8.4 percent growth rate at the start of earnings season. The better-than-expected results were widespread, as all 11 sectors saw earnings growth beat expectations for the quarter. Over the long run, fundamental factors drive market performance, so these solid results were good news for investors.

While fundamental factors were supportive in March, technical factors were challenging. All three major U.S. indices ended the month below their respective 200-day moving averages. This marks the first time that all three indices have finished a month below trend since April of last year, when we were contending with the fallout from the Liberation Day tariff announcements. The 200-day moving average is a widely monitored technical signal, as prolonged shifts above or below this level can signal shifting investor sentiment for an index.

International stocks underperformed in March, with the MSCI EAFE Index down 10.29 percent for the month while the MSCI Emerging Markets Index lost 13.03 percent. International stocks performed well in January and February compared to domestic stocks; however, the large sell-off in March brought both indices into the red for the year. The MSCI EAFE Index lost 1.24 percent for the quarter while the MSCI Emerging Markets Index was down 0.10 percent.

Fixed Income Update: Rising Rates Create Headwinds

Even bonds were down in March, due to rising interest rates and inflation concerns. The 10-year Treasury yield rose from 3.97 percent at the end of February to 4.30 percent by the end of March. Short-term rates also rose notably for the month and quarter. The Bloomberg Aggregate Bond Index lost 1.76 percent in March and 0.05 percent for the quarter. The Bloomberg U.S. Corporate High Yield Index fell 1.18 percent for the month and 0.50 percent in the quarter.

The rising interest rate environment in March was primarily driven by the ongoing war in Iran and concerns about the impact of hostilities on global trade and inflation. Energy prices rose notably in March and could remain high for the foreseeable future, which in turn could lead to further inflationary pressure. Short-term interest rates rose during the month as traders pared back expectations for interest rate cuts from the Federal Reserve.

Returns to Highlight

- Bloomberg U.S. Aggregate Bond Index: down 0.05% in Q1 2026

- Bloomberg U.S. Corporate High-Yield Bond Index: down 0.50% in Q1 2026

At the conclusion of the March Federal Open Market Committee meeting, Fed chair Jerome Powell indicated the Fed will remain data dependent when setting monetary policy at upcoming meetings. He also mentioned it is far too early to say how the war will impact prices and the Fed’s decision-making going forward.

The Takeaway

- Rising interest rates were a headwind for bonds to end the quarter.

- Traders pared back expectations for interest rate cuts due to rising energy prices.

Geopolitical and Economic Update: War with Iran Takes Center Stage

The continued war in Iran was the primary news story throughout the month, and rapidly developing headlines grabbed investor attention and led to choppy returns. The month served as a good reminder that markets face a variety of risks that can unexpectedly develop at any time. While the initial reaction to the strikes at the end of February was muted, markets swung throughout March on war-related headlines and updates.

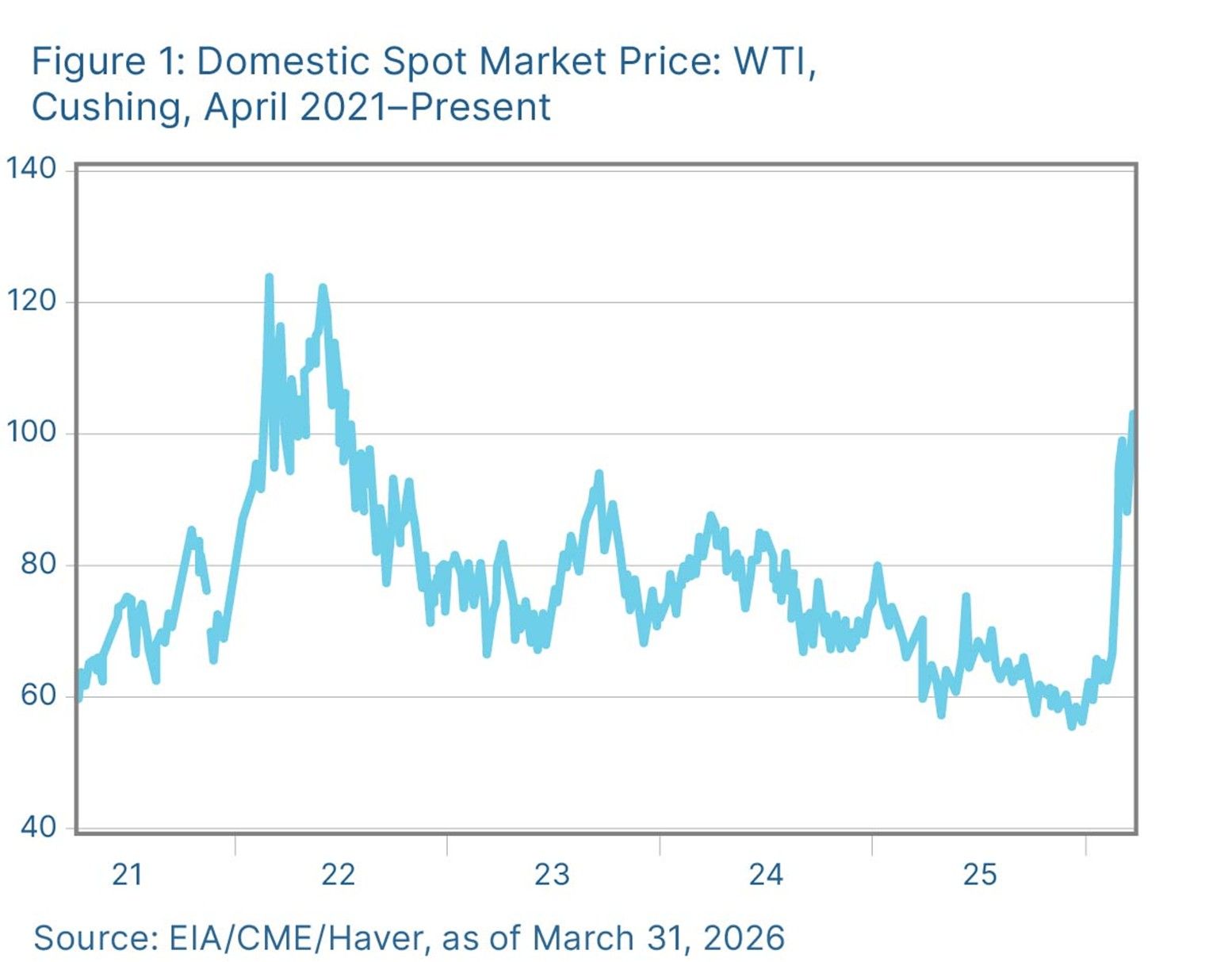

Energy prices remained high and volatile throughout March, with rising crude oil prices in the spotlight. As seen in Figure 1, domestic oil prices rose to over $100 a barrel toward the end of the month, which is the highest we’ve seen since 2022 following the Russian invasion of Ukraine. If higher energy prices persist, this would likely serve as a headwind for future economic growth and lead to rising inflationary pressure.

Figure 1: Domestic Spot Market Price: WTI, Cushing, April 2021-Present

Source: EIA/CME/Haver, as of March 31, 2026

Rising energy prices have already started to have an impact on other areas of the economy. Consumer sentiment fell to a three-month low in March due in part to rising short-term inflation expectations. The survey showed that consumers expect prices to rise by 3.8 percent over the next year, up from 3.4 percent in February. Gas prices were up by roughly $1 on average during the month, and pain at the pump could start to negatively impact discretionary consumer spending in the months ahead.

The Takeaway

- The ongoing conflict in the Middle East captured investor attention during the month.

- The economic impacts from the war are starting to be felt across various sectors of the economy.

Looking Ahead: Shifting Risks

March was a month of shifting risks for investors, which led to rising uncertainty and market volatility. Looking forward, geopolitical risks are expected to remain front and center; however, we may see additional risks to markets materialize as well.

Domestically, we continue to face numerous political risks, as shown by the continued partial government shutdown and the TSA funding impasse during the month. Political uncertainty is expected to ramp up further as we approach the midterm elections in November.

The fundamentals, however, remain relatively solid for now. Companies have shown impressive resilience over the past few years, and continued earnings growth is expected throughout 2026. While headlines can impact markets in the short term, over the long run, fundamentals ultimately drive performance. As long as companies continue to grow, further market appreciation is the most likely path forward.

While March served as a reminder that risks can shift suddenly for markets, the long-term outlook remains solid due to the healthy fundamentals. Given the potential for further short-term disruptions, a well-diversified portfolio that matches investor goals and risk tolerance remains the best path forward for most. If concerns remain, please reach out to us to go over your financial plans.

Disclosure: This material is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Please contact your financial professional for more information specific to your situation. Certain sections of this commentary contain forward-looking statements based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Past performance is not indicative of future results. Diversification does not assure a profit or protect against loss in declining markets. All indices are unmanaged and investors cannot invest directly into an index. The Dow Jones Industrial Average is a price-weighted average of 30 actively traded blue-chip stocks. The S&P 500 Index is a broad-based measurement of changes in stock market conditions based on the average performance of 500 widely held common stocks. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. It excludes closed markets and those shares in otherwise free markets that are not purchasable by foreigners. The Bloomberg Aggregate Bond Index is an unmanaged market value-weighted index representing securities that are SEC-registered, taxable, and dollar-denominated. It covers the U.S. investment-grade fixed-rate bond market, with index components for a combination of the Bloomberg government and corporate securities, mortgage-backed pass-through securities, and asset-backed securities. The Bloomberg U.S. Corporate High Yield Index covers the USD-denominated, non-investment-grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below. One basis point (bp) is equal to 1/100th of 1 percent, or 0.01 percent. Authored by Chris Fasciano, chief market strategist, and Sam Millette, director, fixed income, at Commonwealth Financial Network®. © 2026 Commonwealth Financial Network®

{kind=link}

{kind=link}

{kind=link}

{kind=link}